Here is a scene that happens in almost every Indian household. Salary arrives. Monthly expenses are paid. Whatever is left — put it in an FD. "It is safe. The bank gives guaranteed returns. No tension." This is the thinking of crores of Indian families. And they genuinely believe they are making a smart financial decision.

But here is the truth nobody tells you: Your Fixed Deposit is not building your wealth. It is silently destroying it. Not in one day. Not in one year. But slowly, quietly, over 10 to 20 years.

Your bank will never tell you this. The FD brochure will not mention it. Your relationship manager will not bring it up. So today, we break it down completely — in simple language, with real numbers — so you can finally understand what is actually happening to your hard-earned money.

Why Indians Trust FDs So Much

Our parents and grandparents grew up in an era when FD interest rates were 10%, 11%, even 12% per year. Inflation was lower. There were almost no other investment options available to a common person. Mutual funds were barely known. Stock markets felt like gambling. Banks felt safe and trustworthy.

In that environment, FDs genuinely made sense. But that world no longer exists.

India has changed. The economy has changed. FD rates have dropped dramatically. Inflation has stayed stubbornly high. And the number of better investment options available to every Indian — from any income level — has increased massively.

The FD that worked for your parents is not working the same way for you today. And understanding this difference can completely change your financial future.

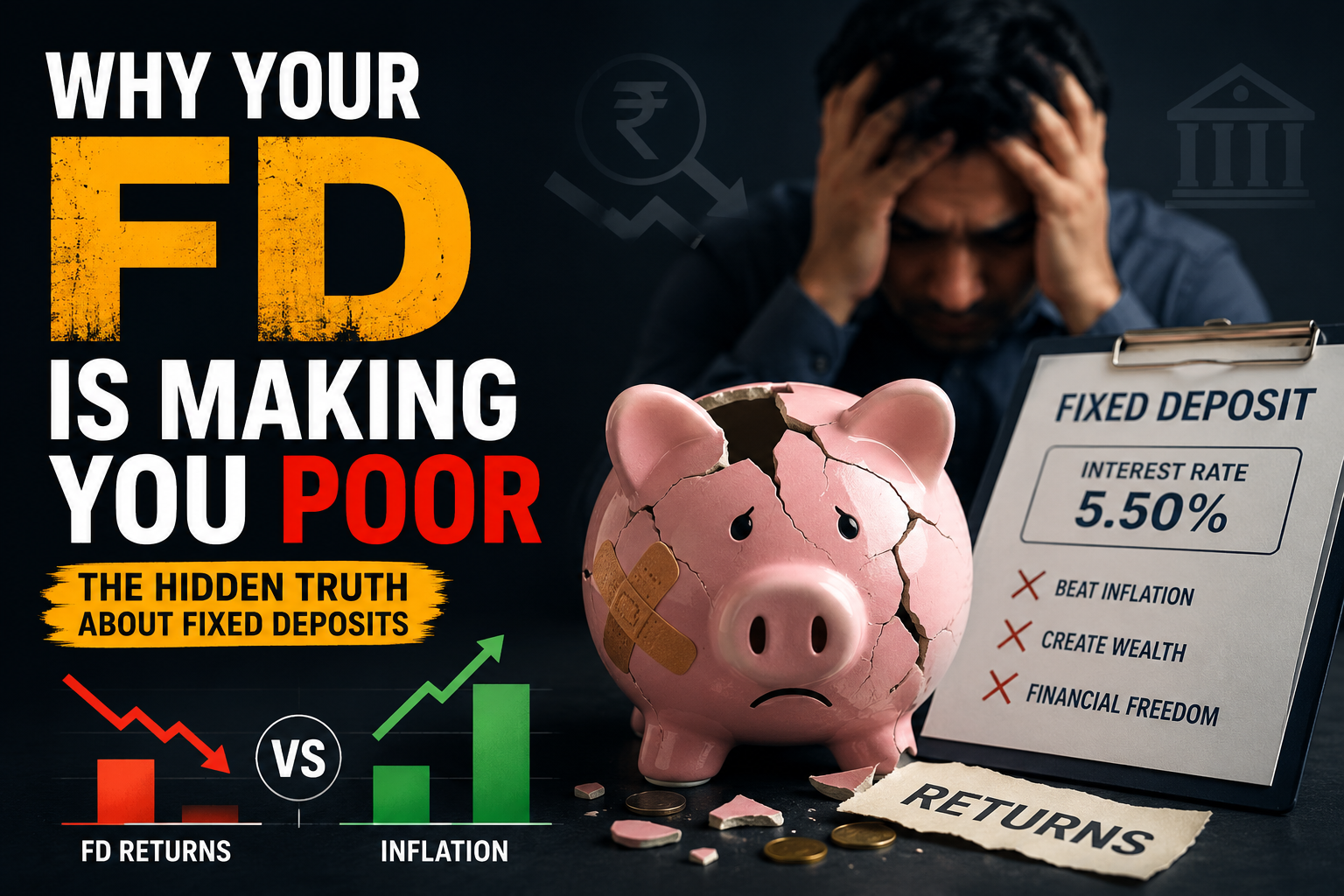

Problem 01: Inflation is Silently Eating Your Returns

This is the most important issue. And it is the most ignored one. Inflation simply means that things get more expensive every year. What costs you ₹100 today will cost ₹105 or ₹106 next year.

India's average inflation rate over the past several years has been around 5% to 6% per year. Most banks offer 6.5% to 7.5% on regular fixed deposits. Now do the simple math:

Your money's actual purchasing power — what it can buy in the real world — is only growing at 1.5% annually. Everything else is just keeping up with rising prices. And this is on a good day when inflation stays at 5.5%.

Groceries, school fees, rent, petrol, medical bills — all rising at 6% to 8% every year. Your FD money is not growing at that speed. You are becoming poorer. Slowly. Silently. Without realising it.

Problem 02: Tax Makes Your FD Return Even Smaller

FD interest is fully taxable in India. Every rupee of interest you earn gets added to your total annual income and taxed according to your slab.

Assume you invest ₹5 lakh in an FD at 7% annual interest:

| Tax Bracket | Interest Earned | Tax Paid | Net Return | Effective Rate |

|---|---|---|---|---|

| 0% (no tax) | ₹35,000 | ₹0 | ₹35,000 | 7.0% |

| 20% bracket | ₹35,000 | ₹7,000 | ₹28,000 | 5.6% |

| 30% bracket | ₹35,000 | ₹10,500 | ₹24,500 | 4.9% |

Now bring inflation back at 5.5%. If you are in the 30% bracket, your effective return after tax is 4.9% — which is already below inflation. You are in negative territory in real terms.

Problem 03: You Are Missing the True Power of Compounding

FDs do offer compounding — quarterly or annually. But at 6% to 7%, the compounding effect is limited. The real magic only reveals itself at meaningfully higher rates over long periods. Look at what happens to the same ₹5 lakh over 20 years:

| Investment Option | Annual Return | Value After 20 Years | Difference vs FD |

|---|---|---|---|

| Fixed Deposit | 7% | ₹19.3 Lakh | — |

| PPF | 7.1% | ₹19.7 Lakh | +₹0.4 Lakh |

| Index Fund (Nifty 50) | 12% | ₹48.2 Lakh | +₹28.9 Lakh |

| Equity Mutual Fund | 14% | ₹68.5 Lakh | +₹49.2 Lakh |

Same starting amount. Same 20 years. But the gap is nearly ₹50 lakh. This is not luck. This is pure mathematics — higher rate compounding over long time = exponentially more wealth.

Problem 04: FD Locks Your Money and Kills Flexibility

When you put money in an FD, it is locked for the chosen tenure. If you need to break it early, the bank charges a premature withdrawal penalty of typically 0.5% to 1% less than the applicable rate.

What if a good investment opportunity appears? What if the market falls and you want to invest more? What if a family emergency requires immediate funds? FD gives you almost zero flexibility to respond to real life situations. And more importantly — money locked in an FD is NOT working for you in better options. This is called opportunity cost. And over 10 to 20 years, this cost is enormous.

Problem 05: Your Life Expenses Grow — FD Returns Stay Fixed

When you put money in an FD at age 30 and plan to use it at age 55, your life looks very different at 55 compared to 30.

- Your children's education costs have grown dramatically

- Medical expenses have increased significantly

- Your lifestyle expectations have risen

- Rent, food, travel — everything costs more

But your FD was locked at 6.5% or 7% when you started it. Lifestyle inflation grows faster than FD returns. This is the gap that catches most middle-class families off guard at retirement.

Problem 06: Banks Profit More From Your Money Than You Do

You deposit money in an FD at 7% interest. The bank takes that same money and lends it as home loans at 8.5%, car loans at 10%, and personal loans at 12% to 18%.

This is not illegal — it is simply how banking works. But the key insight is this: the FD system is designed to benefit the bank far more than it benefits you.

Problem 07-The FD Mindset Keeps You Away From Real Wealth

This is perhaps the biggest hidden cost of all — and it cannot be measured in rupees. People who only invest in FDs never learn about equity, mutual funds, index funds, or SIPs. They stay inside the comfort zone of "safe" investing for their entire working life.

And then they retire with a corpus that looks big in number — but cannot fund the life they expected, because inflation has eroded its real value over decades.

FD thinking keeps you comfortable. It does not make you wealthy. The people who build genuine long-term wealth in India are doing it through equity, compounding, and patient long-term investing — not FDs.

So Should You Never Use FDs?

No. FDs are not useless. They have a specific and limited role in a smart financial plan. The problem was never the FD itself. The problem is using FDs for purposes they were never designed for.

- ✓Use FDs for: Emergency fund (3–6 months expenses), short-term goals under 2 years, capital you absolutely cannot afford to lose, senior citizens needing regular income.

- ✗Do NOT use FDs for: Long-term wealth creation (5–20 year goals), retirement planning, beating inflation over long periods, building a corpus for a comfortable future.

What Smart Indians Are Investing In Instead

1. SIP in Index Funds

An index fund tracks the Nifty 50 or Sensex — it buys all top companies in India proportionally. Very low cost (expense ratio as low as 0.1%), no fund manager bias, and historical long-term return of 12% to 13% CAGR. You can start with as little as ₹500 per month. This is the single most powerful wealth-building tool available to a common Indian.

2. ELSS Mutual Funds

Equity Linked Saving Scheme — tax deduction under Section 80C up to ₹1.5 lakh per year. Shortest lock-in among all 80C options (just 3 years). Historical returns of 12% to 16% over long periods. One investment saves tax and builds wealth simultaneously.

3. PPF — Public Provident Fund

For those who want complete safety: Government-backed (zero risk), current rate of 7.1% — fully tax-free, 15-year tenure with partial withdrawal after year 7. Because the return is tax-free, a 7.1% PPF return is genuinely better than a 7% FD where you pay 20–30% tax on the interest.

4. A Balanced Portfolio

| Goal Type | Time Horizon | Best Option |

|---|---|---|

| Emergency Fund | Immediate | Liquid Fund / Savings Account |

| Short-Term Goal | Under 2 Years | FD or Short-Term Debt Fund |

| Medium-Term Goal | 2–5 Years | Balanced / Hybrid Mutual Fund |

| Long-Term Wealth | 5+ Years | Index Funds + ELSS |

| Tax Saving | Every Year | PPF + ELSS |

Real Numbers: Ramesh vs Suresh

Two friends. Both 25 years old. Both earning ₹40,000 per month. Both decide to invest ₹5,000 every month for 30 years. The only difference — where they invest.

Ramesh — Chose FD

Suresh — Chose Index SIP

Same discipline. Same monthly amount. Same 30 years. But Suresh retires with ₹1.15 crore more than Ramesh. That is not luck. That is mathematics.

A Simple Action Plan Starting Today

-

Audit Your Existing FDs

Check the amount, the rate, and when they mature. Know exactly where your money currently sits.

-

Build Your Emergency Fund

Calculate 3 to 6 months of monthly expenses. Keep only this amount in FD or a liquid savings account.

-

Start Your First Index Fund SIP

Open an account on any reliable platform. Start with whatever you can — even ₹500 per month is a beginning.

-

Start an ELSS SIP for Tax Saving

If you are paying income tax, ELSS saves tax under Section 80C while simultaneously growing your wealth.

-

Open a PPF Account

For additional safe, tax-free savings — especially if you want security alongside your equity investments.

-

Review Every 6 Months

Increase your SIP amount whenever your income increases. Let compounding work harder every year.

The best time to start was 10 years ago. The second best time is today.— Wealthlook | Simple Finance for Common People