Rahul was 27 years old, earning ₹35,000 a month, and completely lost when it came to money.

He had tried reading about stocks once. He spent three hours on it, understood nothing, and closed the tab. He told himself investing was "for rich people" or "for people who understood finance". He kept his savings in a bank account earning 3.5% interest and told himself that was enough.

Then one evening, his colleague Sneha mentioned she had been investing ₹1,500 a month since she was 24. Rahul laughed. "In what? Stocks? That's too risky."

Sneha smiled. "No. Index funds. I don't even think about it. It just runs automatically."

Rahul didn't sleep well that night.

If you're reading this, you might be a little like Rahul. Maybe you've heard the term "index fund" before and moved on, assuming it wasn't for someone like you. Maybe you think investing requires a finance degree, a big salary, or nerves of steel.

It doesn't.

This guide will explain exactly what index funds are, why they are the single best investment tool for beginners in India, and how you can start today — even if you have never invested a single rupee in your life.

By the end of this article, you'll understand more about investing than most people twice your age.

First, Let's Talk About Why Most People Never Start Investing

Before we dive into index funds, let's be honest about something.

Most people in India don't invest. They earn money, spend money, and keep whatever's left in a savings account. And it's not because they're bad with money — it's because investing feels complicated, risky, and exclusive.

Think about it. When you open a financial news channel, you see people in suits shouting about stock prices. When you search "how to invest," you're buried in jargon — P/E ratios, CAGR, alpha, beta, NAV, AUM. It's overwhelming.

So most people do nothing. And doing nothing with money has a very real cost.

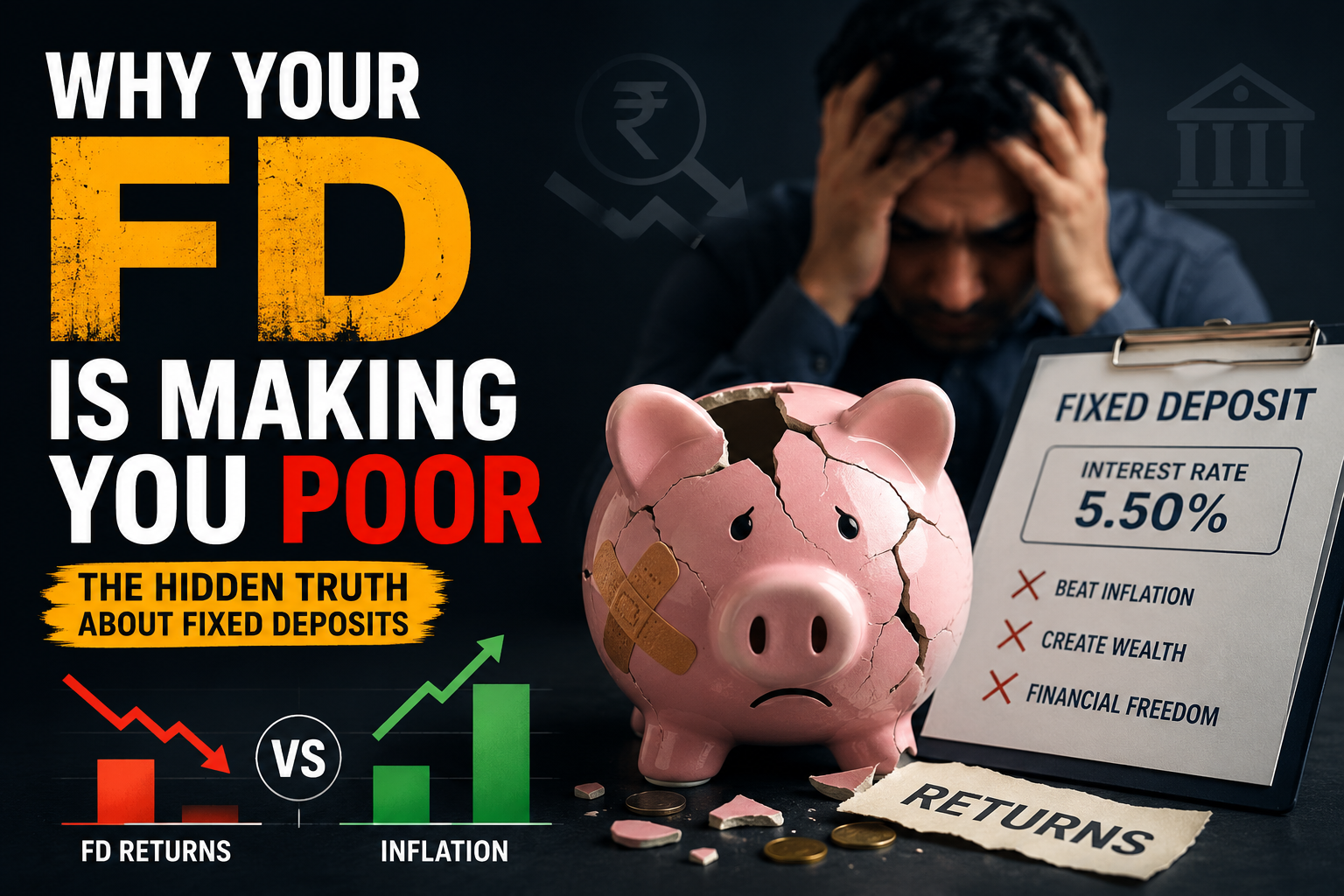

Here's the painful truth: if your money is sitting in a regular savings account earning 3–4% interest, it is actually losing value every year. India's inflation rate averages around 5–6% annually. That means the purchasing power of your money is shrinking every single year it sits idle.

Index funds solve this problem — elegantly, simply, and affordably.

So What Exactly Is an Index Fund?

Let's start from the very beginning.

You've probably heard of the Nifty 50 or the Sensex. These are market indices — essentially, curated lists of the biggest and most important companies on India's stock exchange.

The Nifty 50 tracks the top 50 companies listed on the NSE (National Stock Exchange). We're talking about household names: Reliance Industries, Tata Consultancy Services, HDFC Bank, Infosys, Wipro, Asian Paints, Bajaj Finance — the giants that power the Indian economy.

The Sensex tracks the top 30 companies on the BSE (Bombay Stock Exchange).

Now, an index fund is a mutual fund that mirrors one of these indices. It buys the exact same companies in the exact same proportions as the index it tracks.

So when you invest in a Nifty 50 Index Fund, you are essentially buying a tiny piece of all 50 of India's largest companies — in one single investment.

Reliance goes up? You benefit. TCS announces record profits? You benefit. The Indian economy grows? You benefit.

You're not betting on one company. You're betting on India itself.

Active Funds vs Index Funds: The Battle That Changed Investing Forever

For decades, the investing world was dominated by actively managed mutual funds. These are funds run by professional fund managers — highly paid experts whose job is to pick the best stocks and beat the market.

Sounds great, right? Surely a brilliant expert can pick better stocks than a simple list?

Here's the shocking truth that Wall Street and Dalal Street don't want you to know: most actively managed funds fail to beat their benchmark index over the long term.

Study after study — across decades and across countries — has shown that over a 10 to 15 year period, more than 80% of active fund managers underperform a simple index fund.

Why? A few reasons:

- High fees eat your returns. Actively managed funds charge 1–2% in annual fees. Index funds charge as little as 0.05–0.20%. Over 20 years, that difference in fees alone can cost you lakhs of rupees.

- Human emotion leads to bad decisions. Even experts panic when markets fall and get greedy when markets rise.

- The market is smarter than any one person. Millions of investors, analysts, and algorithms are all competing. It is nearly impossible to consistently outsmart all of them.

This isn't a theory. It's data. And it's why legendary investors like Warren Buffett have famously said that index funds are the best investment most people can make.

In fact, Buffett once made a famous $1 million bet that a simple S&P 500 index fund would beat a collection of actively managed hedge funds over 10 years. He won — easily.

The 5 Reasons Index Funds Are Perfect for Beginners in India

1. They Are Incredibly Simple

You don't need to research companies. You don't need to read annual reports. You don't need to understand technical charts or follow market news daily.

You pick a fund, set up a monthly SIP, and let it run. That's it. A 22-year-old with zero finance knowledge can do this in 15 minutes on their phone.

2. They Give You Instant Diversification

Imagine putting all your savings into one company's stock. If that company collapses — like many did during COVID-19 — you lose everything.

With a Nifty 50 index fund, your money is spread across 50 companies in 13 different sectors — banking, IT, pharma, FMCG, energy, and more. One company failing won't sink your investment.

This is diversification — and it's one of the most fundamental rules of smart investing.

3. The Fees Are Tiny

Most index funds in India charge an expense ratio of 0.05% to 0.20% per year. Compare that to 1.5–2% for actively managed funds.

Let's put that in real numbers. On a ₹10 lakh investment over 20 years:

| Fund Type | Expense Ratio | Fees Paid Over 20 Years | Final Value (12% gross return) |

|---|---|---|---|

| Active Fund | 1.5% | ~₹3,20,000 | ~₹52,00,000 |

| Index Fund | 0.10% | ~₹22,000 | ~₹96,00,000 |

Same money. Same years. Nearly double the result — just from lower fees.

4. They Have a Strong Long-Term Track Record

The Nifty 50 has delivered an average annual return of approximately 12–14% over the last 25 years. This includes the dot-com crash, the 2008 global financial crisis, demonetization, and COVID-19.

Markets fell during all of those events. But they always recovered — and went higher. Every single time.

This is why time in the market beats timing the market.

5. You Can Start With Just ₹100

This is perhaps the most powerful thing about index funds for beginners. You don't need ₹1 lakh or even ₹10,000 to start.

Many platforms allow you to start a SIP (Systematic Investment Plan) in an index fund with as little as ₹100 per month. That's less than two cups of coffee at a café.

What Is a SIP and Why Is It the Smartest Way to Invest?

Back to Rahul's story for a moment.

After that conversation with Sneha, Rahul spent his weekend reading about index funds. He was still nervous. "What if I invest and the market crashes?" he asked Sneha the following Monday.

She explained it like this: "Think of it like buying vegetables at the market. When prices are high, you buy less. When prices fall, you buy more with the same money. A SIP does this automatically — every month, no matter what the market is doing."

A SIP (Systematic Investment Plan) is simply a way to invest a fixed amount into a mutual fund every month — automatically.

It works on a principle called Rupee Cost Averaging. When the market is high, your ₹2,000 buys fewer units. When the market is low, your ₹2,000 buys more units. Over time, your average cost per unit becomes lower than if you had tried to time the market.

SIPs also remove the biggest enemy of investors: emotion. You don't need to decide when to invest. It happens automatically on a set date every month. You can't panic and stop (well, you shouldn't — more on that later).

The Compounding Magic: What ₹2,000 a Month Can Actually Become

Here is where things get genuinely exciting.

Albert Einstein reportedly called compound interest "the eighth wonder of the world." Whether he said it or not, the math is real — and it will change how you think about money forever.

Let's look at what a simple ₹2,000/month SIP in a Nifty 50 index fund can grow into, assuming a conservative 12% annual return:

| Starting Age | Years Invested | Total Money Invested | Estimated Value at Age 55 |

|---|---|---|---|

| 25 | 30 years | ₹7,20,000 | ₹70,00,000+ |

| 30 | 25 years | ₹6,00,000 | ₹37,98,000+ |

| 35 | 20 years | ₹4,80,000 | ₹19,99,000+ |

| 40 | 15 years | ₹3,60,000 | ₹10,11,000+ |

Notice something? The person who started at 25 invested only ₹1,20,000 more than the person who started at 35 — but ended up with ₹50,00,000 more.

That is the brutal, beautiful power of compounding. Time is your most valuable asset. Not money. Not knowledge. Time.

Every year you wait to start investing costs you more than you think.

How to Actually Start: A Step-by-Step Guide

Enough theory. Let's get practical. Here's exactly how to start investing in index funds in India today.

Step 1 — Choose a Platform

You need a mutual fund investment platform. Here are the best options for beginners:

- Groww — Most beginner-friendly app. Clean interface, easy KYC, ₹1 minimum SIP on some funds.

- Zerodha Coin — Best for those who want zero commission direct mutual funds.

- Paytm Money — Simple and trusted, great for first-timers.

- ET Money — Good analytics and portfolio tracking features.

All of these are free to use and regulated by SEBI. Your money is safe.

Step 2 — Complete Your KYC

KYC (Know Your Customer) is a one-time verification process. You'll need:

- PAN Card

- Aadhaar Card

- A selfie

- Bank account details

It takes about 10–15 minutes and is done entirely online. You only need to do this once.

Step 3 — Search for a Nifty 50 Index Fund

Once your account is set up, search for index funds. Here are three excellent, low-cost options:

- UTI Nifty 50 Index Fund — Expense ratio: 0.20%. One of India's oldest and most trusted.

- HDFC Index Fund – Nifty 50 Plan — Expense ratio: 0.20%. Backed by a top AMC.

- Nippon India Index Fund – Nifty 50 — Expense ratio: 0.20%. Solid track record.

All three are excellent choices. Don't overthink it — pick one and start.

Step 4 — Set Up a Monthly SIP

Choose an amount you can invest comfortably every month without affecting your daily life. Even ₹500 is a great start. Set the SIP date to 2–3 days after your salary credit date so the money moves automatically before you can spend it.

Step 5 — Set It and (Almost) Forget It

Once your SIP is running, your job is mostly done. Check your portfolio once every 3–6 months. Increase your SIP amount whenever your income increases. And above all — don't stop your SIP when the market falls.

The Mistakes That Can Destroy Your Returns (And How to Avoid Them)

❌ Mistake 1: Stopping Your SIP During Market Crashes

When the market falls 20–30%, every instinct tells you to stop investing. This is the worst thing you can do. Market dips are sales. Your ₹2,000 buys more units when markets are down. Stopping is like leaving a store during a 30% discount sale.

What to do instead: Keep your SIP running. If possible, increase it temporarily during crashes.

❌ Mistake 2: Checking Your Portfolio Every Day

Index fund investing is a long-term game. Daily price movements are noise. Constantly checking your portfolio leads to emotional decisions that hurt returns.

What to do instead: Set a quarterly reminder to review your portfolio. That's it.

❌ Mistake 3: Waiting for the "Perfect" Time to Start

"I'll start when the market corrects." "I'll start next month when I get my bonus." These are lies we tell ourselves. No one can predict the market. The best time to start was yesterday. The second-best time is today.

What to do instead: Start now with whatever amount you have. Increase later.

❌ Mistake 4: Investing Money You Might Need Soon

Index funds are for money you won't need for at least 5–7 years. Don't invest your emergency fund or money earmarked for next year's expenses.

What to do instead: Build a 3–6 month emergency fund in a liquid fund or high-yield savings account first. Then invest.

Rahul's Story: One Year Later

It's been 14 months since Rahul's conversation with Sneha.

He started with a ₹1,500/month SIP in UTI Nifty 50 Index Fund. It felt small. Almost embarrassingly small. But he set it up on a Sunday afternoon on Groww, and the next month, it just... ran. He didn't have to do anything.

In month four, the market fell sharply. Rahul's portfolio was down 11%. He felt the urge to stop. He called Sneha instead. She said, "Don't touch it. This is when it matters most."

He didn't touch it.

By month 14, his portfolio had recovered and was up 16% from his total investment. He had invested ₹21,000. His portfolio was worth ₹24,360.

More importantly, he understood something he hadn't before: wealth isn't built in one big moment. It's built in small, consistent actions over time. ₹1,500 a month. Month after month. That's it.

Last week, he increased his SIP to ₹3,000.

Frequently Asked Questions About Index Funds

Are index funds safe?

No investment is 100% risk-free. Index funds carry market risk — their value goes up and down with the market. However, because they hold 50+ companies across multiple sectors, they are far less risky than investing in individual stocks. Over long periods of 10+ years, Nifty 50 index funds have never given negative returns historically.

How much should I invest each month?

Start with whatever you can afford without financial stress. Even ₹500/month is a great beginning. The key is consistency, not amount. As your income grows, increase your SIP.

What is the minimum investment?

Most index funds allow a minimum SIP of ₹100–₹500/month. Some platforms like Groww allow even lower amounts on certain funds.

Do I pay tax on index fund returns?

Yes. Long-term capital gains (LTCG) on equity mutual funds held for more than 1 year are taxed at 10% on gains above ₹1 lakh per year. Short-term capital gains (held less than 1 year) are taxed at 15%. For most long-term investors, the tax impact is minimal.

Can I withdraw my money anytime?

Yes. Index funds are liquid — you can redeem your investment anytime. However, for best results, treat your investment as long-term (7–10+ years) and avoid withdrawing unless absolutely necessary.

The Bottom Line: Your Wealth Journey Starts With One Small Step

Index funds are not complicated. They are not exclusive. They are not just for the wealthy or the financially educated.

They are, simply put, the most accessible, most reliable, and most beginner-friendly way to build long-term wealth in India today.

You don't need to understand the stock market. You don't need to watch CNBC. You don't need a financial advisor charging you ₹5,000 an hour.

You need:

- A PAN card ✅

- A bank account ✅

- 15 minutes to set up an account ✅

- ₹500–₹1,000 a month ✅

- Patience ✅

That's the entire formula.

Rahul figured it out at 27. Sneha figured it out at 24. The earlier you start, the more time your money has to work for you.

Open Groww or Zerodha Coin today. Search "Nifty 50 Index Fund." Start a SIP. Even if it's just ₹500.

Your future self will thank you.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Please consult a registered financial advisor before making investment decisions. Mutual fund investments are subject to market risks. Past performance does not guarantee future results.