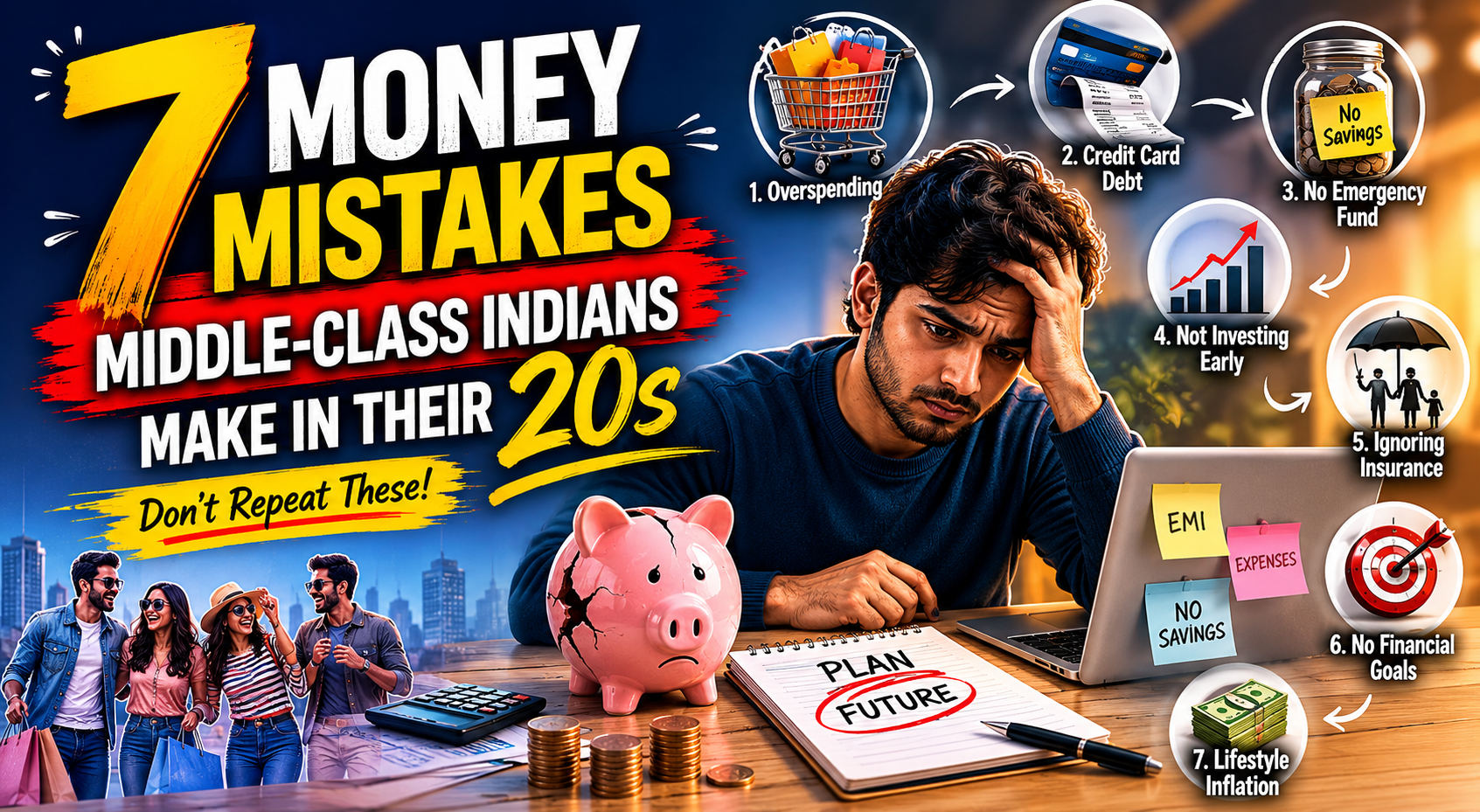

7 Money Mistakes Middle-Class Indians Make in Their 20s

Your 20s are the most important financial decade of your life. A few smart decisions now can change everything later.

Most people think wealth creation is something that happens after 35 or 40. After the promotions. After the big salary. After settling down. That is one of the most expensive beliefs you can hold.

Here is what nobody tells you when you are 22 or 24 or 26 and just starting your first job: your 20s are the single most important financial decade of your entire life. Not your 40s. Not your 50s when you finally have "enough money to invest." Your 20s.

This is the decade where your habits are formed and hardened. Where your lifestyle choices become permanent patterns. Where your relationship with money — healthy or toxic — gets established for the next 30 years. Where the compounding clock either starts ticking in your favor or quietly ticks against you.

The difference between a middle-class person who retires comfortably at 55 and one who is still financially stressed at 60 is rarely income. Most of the time, it comes down to a handful of decisions made — or avoided — in their 20s.

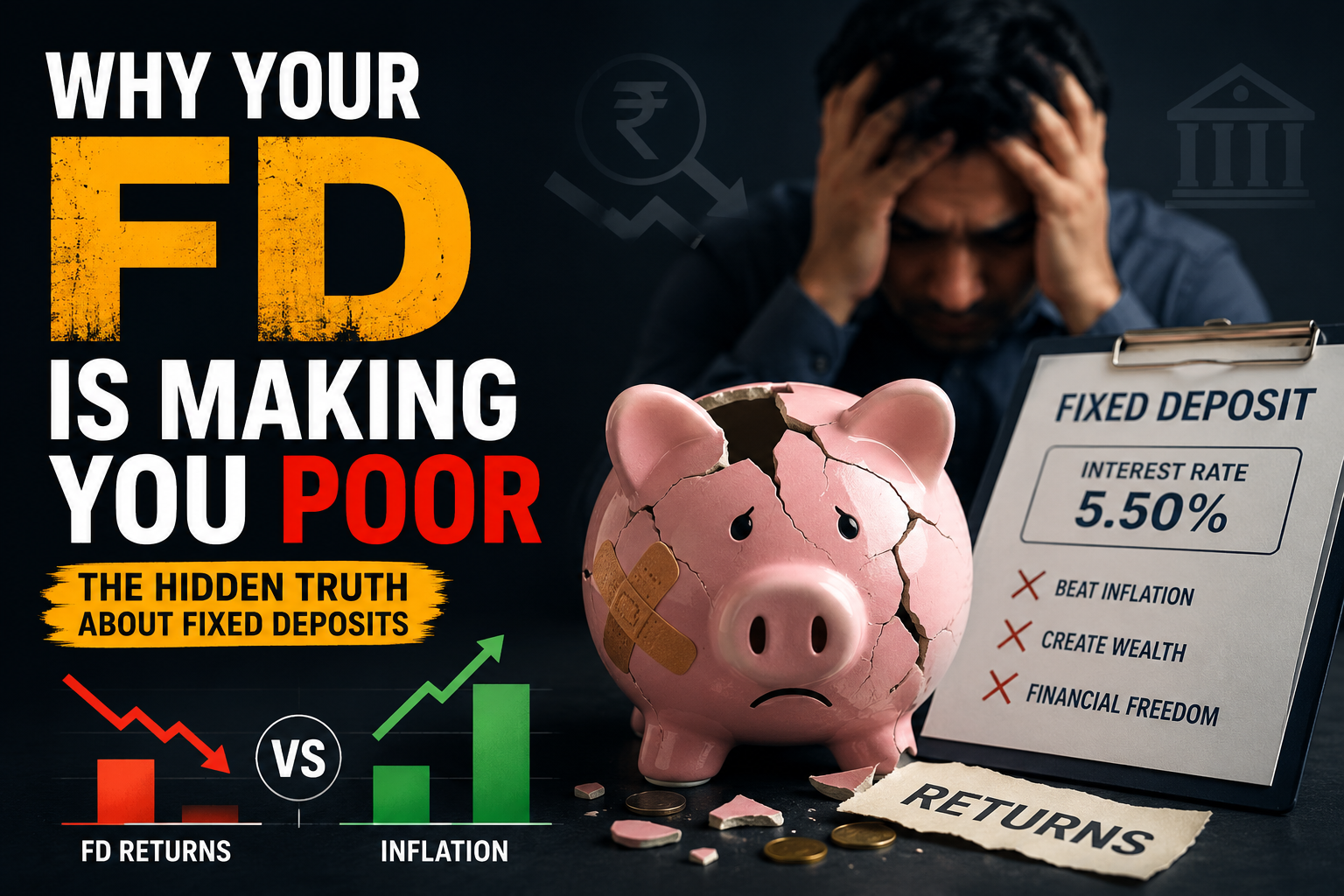

Delaying Investing for "Later"

This is the single biggest financial mistake that most young Indians make. And also the most underestimated one. The thinking usually sounds like this:

- My salary is too low right now. Let me wait until I earn more.

- I will start investing after my next promotion.

- I need at least ₹10,000 to ₹15,000 per month before I start.

- I need to enjoy my 20s first. Investing can wait.

All of these thoughts feel reasonable in the moment. None of them are financially sound. Here is the reality: investing is far more about time than it is about amount. The single most valuable ingredient in wealth creation is not a large salary, not a high return, not a brilliant stock pick. It is time.

| Investor | Start Age | Monthly SIP | Total Invested | Value at 55 (12%) |

|---|---|---|---|---|

| Priya (started early) | 22 | ₹3,000 | ₹11.88 Lakh | ₹1.70 Crore |

| Rahul (waited) | 32 | ₹10,000 | ₹27.60 Lakh | ₹1.50 Crore |

Priya invests less than half the total amount. She invests ₹3,000/month vs Rahul's ₹10,000/month. And she still ends up with more money at 55. The only difference is ten years of compounding.

Every year of delay does not just push your start date back — it exponentially reduces your final wealth. The first years of investing are the most valuable because every rupee invested at 22 has 33 years to compound.

What to Do Instead

Start today. Even ₹500 or ₹1,000 per month. The amount matters far less than the habit and the starting date. Open a mutual fund account and set up an automatic SIP. You do not need to understand everything before you start — the act of starting is worth more than years of waiting.

Depending Fully on One Salary

There is a particular kind of financial anxiety that comes from knowing that your entire life — rent, food, loans, family support, savings, everything — depends on one source of income that can disappear with a single HR email.

Most young Indians in their 20s live in exactly this situation. One job. One salary. One income stream. And complete dependency on it. Layoffs happen suddenly. Industries get disrupted. Health issues arise. We saw this clearly during COVID when lakhs of salaried employees lost their income overnight with zero backup.

Modern wealth creation — and basic financial stability — requires thinking beyond the monthly salary. This does not mean quitting your job. It means building additional income streams gradually, alongside your regular job.

The options available to an educated, skilled young Indian in 2026 are genuinely enormous. Freelancing in your area of expertise. Content creation. Teaching a skill online. Affiliate marketing. Investing in dividend-paying assets. Even an extra ₹5,000 to ₹10,000 per month from a side activity builds confidence, expands skills, and reduces dependency on a single employer.

What to Do Instead

Identify one skill you already have that someone else would pay for. Start small — one project, one client, one piece of content. Think of building a second income stream the same way you think about a SIP: start small, be consistent, and let it grow over time.

Buying Expensive Things to Impress Others

EMI culture has fundamentally changed how young Indians think about money. What used to require saving has been replaced by the false convenience of "easy monthly installments." And combined with constant social comparison on social media, this has created a generation of young earners spending their future wealth on present appearances.

The problem is not spending money on good things you genuinely want. The problem is sacrificing your financial future — the compounding that should be happening right now — for temporary social validation from people who are mostly not paying attention anyway.

Every ₹50,000 spent impulsively at age 24 is not just ₹50,000 gone. At 12% compounding over 30 years, that amount would have become approximately ₹15 lakh by the time you are 54. That phone upgrade cost you not ₹20,000 but the ₹6 lakh it would have become.

This is not about living miserably or never spending on yourself. It is about being genuinely conscious about what you are spending and why. The question worth asking before any significant purchase is not "can I afford the EMI?" but "is this worth more to me than what it could become if I invested it?"

What to Do Instead

Create a simple monthly budget with a specific amount for discretionary spending — and stick to it. For large purchases, wait 30 days before buying. If you still genuinely want it after 30 days, buy it thoughtfully. Most impulse purchases lose their appeal quickly when you pause and reflect.

Ignoring Emergency Funds

This mistake might not feel urgent when nothing has gone wrong. But it is one of those things where you only truly understand its importance in the moment when you desperately need it and do not have it.

Medical emergencies do not send advance notice. Job losses happen unexpectedly. Family situations require sudden large sums. Without a financial buffer, each of these situations forces a set of terrible choices.

| No Emergency Fund → Response | Financial Cost |

|---|---|

| Credit card debt | 36–42% annual interest |

| Personal loan | 14–18% annual interest |

| Break investments early | Lost compounding + penalties |

An emergency fund is the financial equivalent of a seatbelt — you do not notice it when everything is fine, and you are enormously grateful for it when something goes wrong. A basic emergency fund should cover 3 to 6 months of your actual monthly expenses.

Keep it somewhere accessible — a high-interest savings account, a liquid mutual fund, or a short-term FD. Easy to access within 24 to 48 hours if needed, but not so easy that you dip into it for non-emergencies.

What to Do Instead

Start building your emergency fund before you start investing aggressively. Even setting aside ₹2,000 to ₹3,000 every month specifically for this purpose will get you there in 12 to 18 months. Treat it as a non-negotiable monthly expense, not an optional saving.

Avoiding Health Insurance Early

If there is one mistake on this list that young Indians most consistently and confidently make, it is this one. The reasoning is understandable — you are 23 or 25, you are healthy, you rarely get sick. Health insurance feels like paying for something you will never use.

But this thinking misunderstands what insurance is actually for. Insurance is not bought for the situations you expect. It is bought for the situations you cannot predict. In India, where healthcare costs rise at 14% to 15% annually, a single serious hospitalization can generate a bill that takes years of savings to recover from.

A week-long hospitalization in a decent private hospital in any major Indian city can cost ₹3 lakh to ₹8 lakh or more. Without insurance, this comes directly from your savings — destroying years of disciplined investing in a single medical event.

| Why Buy Early | Benefit |

|---|---|

| Lower premiums | ₹10L cover at 24 costs ~₹7,000/year vs ₹22,000/year at 40 |

| Waiting periods finish early | Pre-existing condition coverage by age 26–28 |

| No denial risk | Lock in coverage before health issues develop |

What to Do Instead

Buy a basic individual health insurance policy of at least ₹5 lakh cover as soon as you start earning — ideally ₹10 lakh. Do not depend solely on your employer's group health insurance. It ends when your employment ends, which is exactly when you might need it most.

Using Credit Cards Without Discipline

Credit cards are genuinely useful financial tools when used correctly. The problem is not credit cards themselves — the problem is using them without understanding exactly what the costs of careless usage are.

The most dangerous trap is the minimum payment option. Every statement shows a "minimum amount due" — typically 5% of the outstanding balance. Paying just this minimum feels responsible. But the remaining 95% attracts interest at 36% to 42% per year — among the highest interest rates of any financial product in India.

- Paying only minimum dues on a ₹30,000 balance takes years to clear and costs significantly more in interest.

- Owning multiple cards and losing track of total spending across them.

- Converting everyday purchases into EMIs without checking the effective interest rate.

- Treating the credit limit as a spending budget rather than an emergency facility.

Used carelessly, a credit card is one of the most expensive financial products in existence. 36% to 42% annual interest on unpaid balances makes it practically impossible to build wealth simultaneously.

What to Do Instead

Use a maximum of one or two credit cards. Pay the full outstanding balance every single month — not the minimum, the full amount. Set up auto-pay if possible. Never spend on a credit card what you could not immediately afford from your bank account. Used this way, a credit card is a genuinely useful tool.

Not Learning About Money

This is the mistake that makes all the other mistakes worse — and more likely to happen in the first place. The Indian education system is excellent at teaching mathematics, science, and engineering. But it teaches almost nothing about the financial realities of adult life.

Most Indian graduates enter their first jobs with no practical understanding of how income tax works, what mutual funds are, how insurance functions, what a credit score is and why it matters, or what retirement planning actually requires. They are handed a salary and left to figure it out — usually by making expensive mistakes first.

Financial literacy is one of the highest-return investments you can make in your 20s. It costs almost nothing — mostly time — and the compounding returns on knowledge are as real as the compounding returns on money.

The specific concepts worth learning are not complex or intimidating. What a mutual fund is and how SIPs work. How income tax slabs function and which deductions are available. The difference between term insurance and investment-linked insurance. What a credit score is and how to build a good one. The basics of retirement planning and why starting early matters.

None of these require a finance degree. They require an hour a week of focused reading, listening to a good personal finance podcast, or following credible financial content creators.

What to Do Instead

Commit to learning one financial concept per week. Read one good personal finance book written for the Indian context. Follow credible financial educators. The goal is not to become an expert — it is to make informed decisions about your own money instead of accidentally defaulting to the most common and most expensive choices.

Simple Habits That Build Wealth in Your 20s

The seven mistakes above paint what to avoid. Here is what actually works — and it is simpler than you think.

Start SIPs Early

Even ₹500/month at 22 beats ₹5,000/month at 32. Time is the variable that matters most.

Track Monthly Expenses

You cannot manage what you cannot see. A simple spreadsheet creates enormous clarity.

Avoid Unnecessary EMIs

Every EMI reduces your monthly cash flow and your ability to invest. Think twice before committing.

Build Emergency Savings

3–6 months of expenses in a liquid account before aggressive investing. Non-negotiable.

Invest in Your Skills

Your earning capacity is your most important financial asset in your 20s. Grow it continuously.

Think Long Term

Extend your time horizon to decades. The right decisions become clearer. The sacrifices feel smaller.

Your 20s Are Not a Trial Run. They Are the Most Important Financial Decade of Your Life.

Most middle-class people do not struggle financially because they earn less. They struggle because of delayed decisions and repeated money mistakes made early. Start before you feel ready. The cost of waiting is enormous.